12-March-2020

English

5-December-2019

English, PDF, 297kb

5-December-2019

English, PDF, 454kb

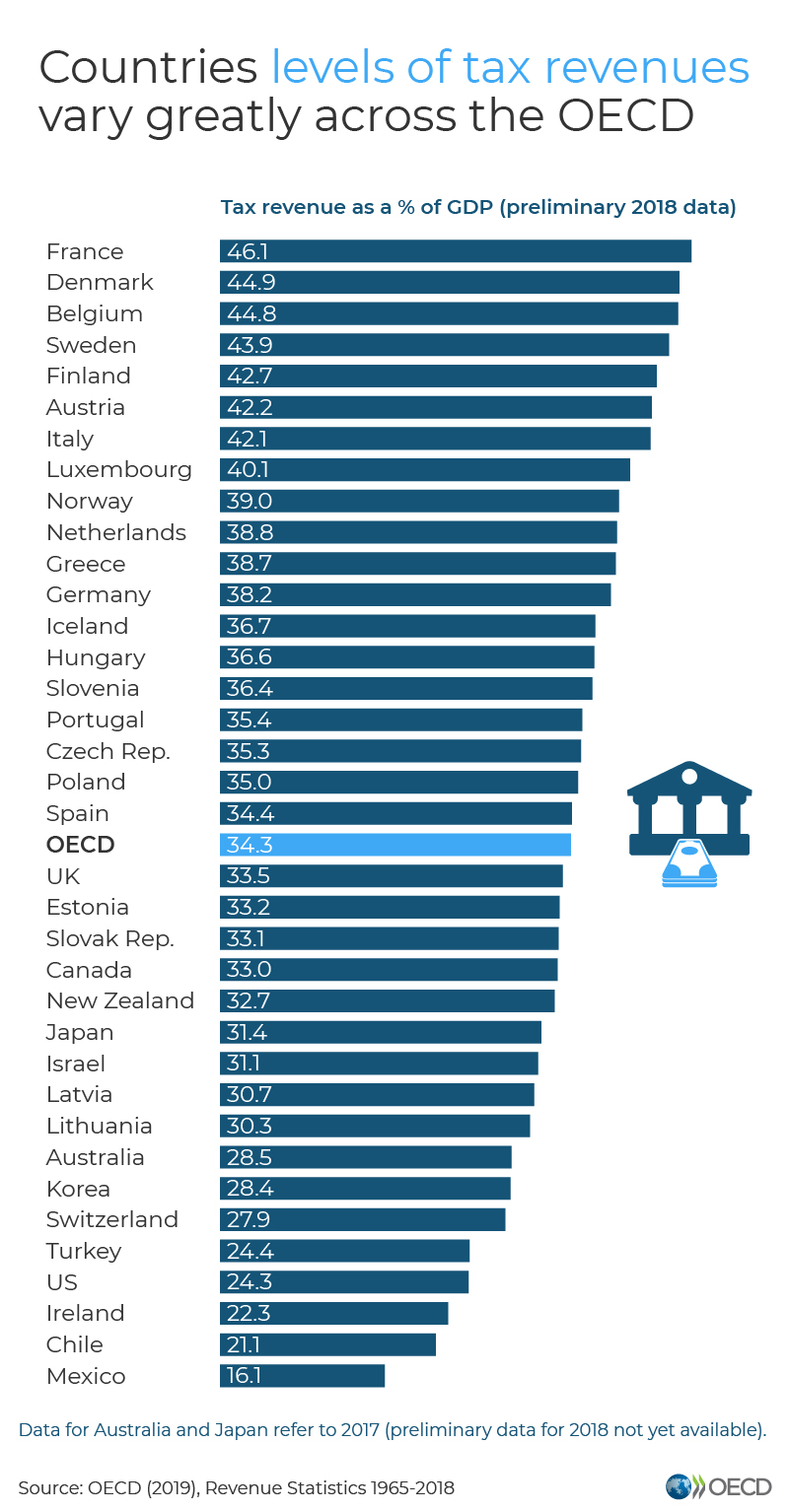

Il rapporto annuale OCSE sulle entrate pubbliche, Revenue Statistics 2019, rileva che in Italia il rapporto gettito fiscale/PIL non è cambiato tra il 2017 e il 2018. Il gettito fiscale in rapporto al PIL si è attestato al 42.1%. Il valore corrispondente per la media OCSE ha registrato un lieve aumento di 0,1 punto percentuale, dal 34.2% al 34.3%.

15-October-2019

English, PDF, 1,379kb

This country note explains how the United States taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

15-October-2019

English, PDF, 1,080kb

This country note explains how Australia taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

15-October-2019

English, PDF, 1,176kb

This country note explains how the Czech Republic taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

15-October-2019

English, PDF, 1,065kb

This country note explains how the People's Republic of China taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

15-October-2019

English, PDF, 1,149kb

This country note explains how Argentina taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

15-October-2019

English, PDF, 1,107kb

This country note explains how Switzerland taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

15-October-2019

English, PDF, 1,053kb

This country note explains how the Slovak Republic taxes energy use. The note shows the distribution of effective energy tax rates across all domestic energy use. It also details the country-specific assumptions made when calculating effective energy tax rates and matching tax rates to the corresponding energy base.

{kind=link}